Latest Technology News

Innovative Systems for Cleaning and Reprocessing Plastic Films

Plastic waste continues to grow across many industries.…

Database Optimization: Boost Performance, Improve Efficiency, and Unlock the True Power of Your Data

What is Database Optimization? In today’s fast-paced digital…

Perfect Your Swing Anytime With Immersive Golf Technology

Perfecting your golf swing no longer depends on…

Top 8 AI-Powered Photo Enhancers for Travel Ads and Digital Campaigns

In the competitive world of digital marketing, especially…

How to Stay Updated with Gaming News: Tools, Feeds, and Communities

The gaming industry moves at an incredible pace,…

How to Optimize Linux for Gaming: Hardware, Software, and Performance Tips

Gaming on Linux has evolved from a niche…

Unlocking Efficiency with Data Governance as a Service

In today's data driven world, organizations face mounting…

How AI Voice Technology Is Changing the Way We Create Content

Content creation has evolved dramatically in the past…

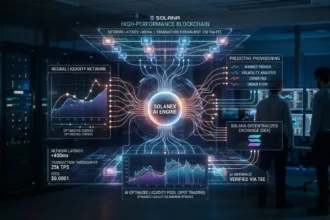

Technical Analysis of the Solanex AI Protocol

The evolution of decentralized finance has reached a…